Should I open a 529 plan?

A 529 plan is a great tool for saving for college. So should you open a 529 plan for your loved ones?

According to NerdWallet, there are two different kinds of 529 plans.

- 529 Savings Plan

- 529 prepaid plan

529 college savings plans are the most common type. Investments grow tax-free and can be withdrawn tax-free for educational expenses like tuition, room, and board, and required textbooks.

529 prepaid plans let you prepay part or all of in-state public tuition, locking in the tuition at the time of payment.

NerdWallet

Every state has their own 529 plans. NerdWallet offers a list of the plans in each state and whether the plan offer any tax incentive. I live in Texas and unfortunately Texas does not offer any tax incentive.

Even if they do, with a pharmacist salary, I doubt that I and my wife qualify for such an incentive.

I am left with two options, go with the Texas College Savings Plan or go with another plan. One thing to point out is that you do not need to sign up for the plan that your state offers, you can do a compare and contrast and pick the plan that is right for you.

Texas College Savings Plan

The first thing that I liked when browsing through the Texas’ 529 plan is its tuition estimation tool

The tool break down into your child’s age and whether he/she is going to a public or private school.

My daughter is now 7 years old and by using the tool, I need to save $124,553 for my daughter’s education. If we switched gear and went with a private school, the price tag swelled up to $274,469 dollars. Understandably, this is just an estimate and we may not even need that much or possibly more?

A few highlight from the Texas College Savings Plan A.K.A. the Texas 529 Plan.

- A minimum contribution of $25 to get started

- No tax incentive as offered by other states

- Tax-free withdrawal

- Different investment portfolios dependent on risk tolerance, time horizon, current financial situation, and other variables

- Automatic investing option

- Total fees for portfolios range from 0.60%-1.00%

529 Plan Features

- You can use the 529 plan account to pay for qualified higher education expenses

- A beneficiary can be your child, grandchild, relative, friend, spouse, or even yourself

- Because the account is in your name, you control over when and how the savings are used

- If the beneficiary receives a scholarship, you can withdraw up to the amount of the tax-free scholarship without penalty (income tax excluded on earnings)

- May be used for k-12 tuition ($10,000), student loan repayment or participation in a registered apprenticeship program

- Tax-free growth earnings are not subject to federal or state tax when used for qualified education expenses

- Tax-free withdrawal

- Gifts to 529 plans are partially exempt from federal gift tax ($15,000 annually up to $75,000 over a five-year period or $30,00 or up to $150,000 for married couples)

Qualified expenses

- Fees, books, supplies, and required equipment

- Certain room and board expenses

- Computer and computer software

- Internet access and related services

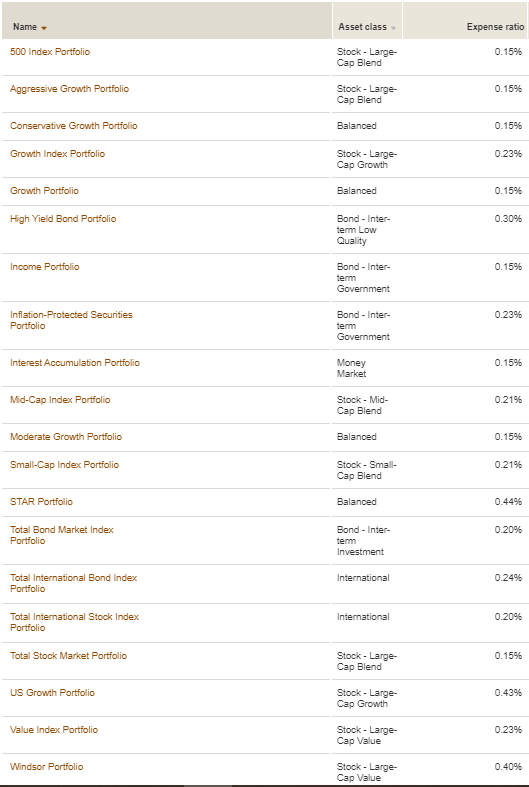

The Vanguard 529 Plan

Aside from the Texas plan, I looked at an alternative option from Vanguard.

The Vanguard 529 plan is sponsored by the state of Nevada and offers two different mode of investments to choose from.

- Age-based portfolios: 0.15% expense ratio

- Individual portfolios: 0.15%-0.44

The downside to the Vanguard 529 Plan is the $3,000 minimum requirement to get started.

If you don’t want to or not able to open the Vanguard 529 plan, you can choose the College Savings Iowa 529 Plan.

The Iowa 529 Plan charges a 0.20% expense ratio, slightly more than the Vanguard plan but you only need $25 to get started similar to the Texas 529 plan.

The plan features 4 age-based savings tracks and 10 individual portfolios.

In contrast, the Vanguard 529 plan features 3 age-based option and 20 individual portfolios.

Age-based versus Individual Portfolios

In a way age-based is very similar to a Vanguard target date funds or any other company’s target date funds.

There are 3 age-based options to choose from:

- Conservative

- Moderate

- Aggressive

The options are based on your risk tolerance. One of the advantages of the age-based portfolios is that the plan will reallocate holdings automatically as your child approaches college age.

The options will shift from more stocks to more bonds as the child reaches age 18.

Vanguard standardized their age-based portfolio in these 4 funds:

- Total US Stock Market Index

- Total International Stock Market Index

- Total US Bond Index

- Total International Bond Index

On the other hand, if you went with the custom option, the 20 individual funds you can choose from is the usual Vanguard favorites.

You are allowed to choose up to 5 funds for the custom track. These funds range from the total stock index, S&P 500, small caps, large caps, total bond index funds, and also its international equivalents.

How much to contribute?

According to CNBC, Americans have $371.5 billion saved among 14 million 529 plans.

That’s significant because CNBC project that average college tuition will increase 3% a year.

Assuming that there are 17 years from birth to college enrollment, parents should be saving $250 a month for an in-state public college, $450 a month for out-of-state public college, and $550 a month for private nonprofit college.

As with any form of investment, due to compound interest, your greatest asset is your time. The sooner you start saving, the more interest you will earn.

Final Thoughts

I decided to choose the Vanguard 529 plan over the Texas plan because of cost and Vanguard’s broad offerings. I decided to keep things simple and go with a two-fund portfolio comprising of the total stock market index fund and the total bond index fund at a 90% to 10% ratio.

Of note, I just opened a 529 plan now when my daughter is turning 8 years old next month. We have 10 years to contribute toward her 529 plan. It should be pointed out that it’s more ideal if you start the plan when your child is just born to take advantage of compound interest. It’s better late than never so I am starting now but the sooner the better. Just like how I opened m Roth IRA account last year when I could have started when I was in my 20s.

If you’re planning for the future and worry about paying for your child’s tuition then a 529 plan is right for you. College tuition is getting more and more expensive every year. A 529 plan is another tax advantage tool we can utilize to unburden our children from college student loans as they enter the workforce or enroll in graduate or professional programs.

It’s important to know that 529 plans are intended for education expenses only. If you use the funds for anything else then you’ll be subject to 10% penalty and income tax on earnings.

However, after the age of 59 1/2, you will only need to pay income taxes on the funds if you wish to use it for non-education expenses.

Save your child from massive loans but starting a 529 plan today!

Pingback: Does 7 Baby Steps by Dave Ramsey Work? - Pharmacist Money Blog